BNS Volatility Model¶

This tutorial calibrates the BNS stochastic-volatility model (Barndorff-Nielsen and Shephard) and its two-factor extension BNS2 to an implied volatility surface, using the same workflow as the Heston tutorial in Volatility Surface.

BNS is structurally different from Heston. The variance process is a non-Gaussian Ornstein-Uhlenbeck process driven by a pure-jump Lévy process (Gamma-OU in this implementation), and the leverage effect is introduced by correlating the same jumps into the log-price.

Single-factor BNS¶

BNSCalibration fits five parameters to the surface:

| Parameter | Description |

|---|---|

v0 |

Initial variance (\(v_0\)) |

theta |

Long-run variance (\(\theta = \lambda / \beta\)) |

kappa |

Mean reversion speed of the variance process |

beta |

Exponential decay rate of the BDLP jump-size distribution |

rho |

Leverage parameter (correlation between jumps in variance and log-price) |

The BDLP intensity is set as \(\lambda = \theta \beta\) so that the stationary mean of the Gamma-OU variance process equals \(\theta\). This gives the same \((v_0, \theta)\) parameterisation as Heston.

Because the variance is built from positive jumps and exponential mean reversion, it stays positive by construction. No Feller-style penalty is needed.

How BNS fits the surface¶

The mechanism that produces a smile in BNS is structurally different from Heston. Heston relies on a diffusive volatility-of-variance \(\sigma\) for the wings and a spot-variance correlation \(\rho\) for the skew, both accumulating as \(\sqrt{T}\). BNS instead injects discrete jumps directly into the variance process: each jump in \(v_t\) is mirrored, scaled by \(\rho\), into the log-price. The wing thickness is governed by the jump-size distribution (controlled by \(\beta\)) and the skew by \(\rho\).

A consequence of this structural difference is that the calibrator often settles at a small \(\kappa\) together with a large \(\theta\). The time scale of mean reversion is \(1/\kappa\), so when \(\kappa\) is small the variance process barely relaxes towards \(\theta\) over the calibration horizon and stays close to \(v_0\) throughout.

In that regime \(\theta\) is only weakly identified by the surface and the optimizer can move it freely as long as the jump-driven smile dynamics are preserved. The headline number to read in the output is \(v_0\), which sets the at-the-money level.

Calibrated parameters¶

The fit uses the VolModelCalibration two-stage optimiser: L-BFGS-B for basin search, followed by trust-region reflective on the residual vector with parameter bounds.

ftol termination condition is satisfied.

{

"variance_process": {

"rate": 0.09654620991832212,

"kappa": 3.7918136142969967,

"bdlp": {

"intensity": 1.0238928441533703,

"jumps": {

"decay": 3.8764373402256695

}

}

},

"rho": -0.2957691167993344

}

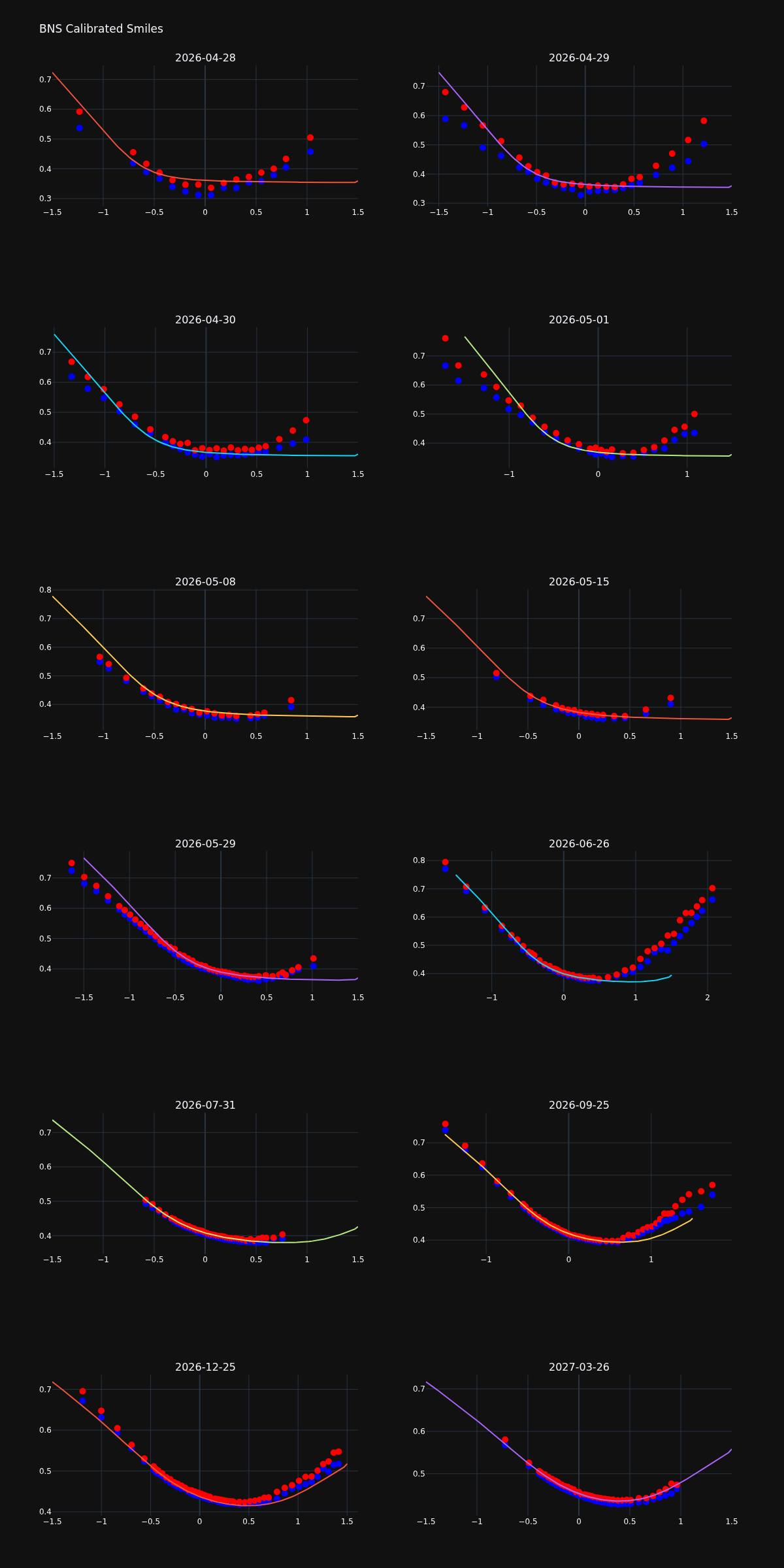

The fit is good for medium and long maturities and visibly off at the front expiries. This is the same short-maturity gap seen for Heston and Heston-jump-diffusion.

The cause here is structural: BNS adds jumps, but they live in the variance process, not directly in the log-price. The jump-driven contribution to the log-price is bounded by the size of the variance jumps multiplied by \(|\rho|\), which is small for short tenors. A model with explicit jumps in the log-price (such as HestonJ) or a rough volatility model is better suited to the steep short-term skew observed in crypto markets.

Code¶

import json

from docs.examples._utils import FIXTURES, assets_path, print_model

from quantflow.options.calibration import BNSCalibration

from quantflow.options.pricer import OptionPricer, OptionPricingMethod

from quantflow.options.surface import VolSurface, VolSurfaceInputs, surface_from_inputs

from quantflow.sp.bns import BNS

# Load a saved volatility surface snapshot and build the surface

with open(FIXTURES / "volsurface_btc.json") as fp:

surface: VolSurface = surface_from_inputs(VolSurfaceInputs(**json.load(fp)))

surface.bs()

surface.disable_outliers()

# Create a BNS pricer with initial parameters

pricer = OptionPricer(

model=BNS.create(vol=0.5, kappa=1.0, decay=10.0, rho=-0.2),

method=OptionPricingMethod.COS,

)

calibration: BNSCalibration[BNS] = BNSCalibration(

pricer=pricer,

vol_surface=surface,

moneyness_weight=0.5,

)

result = calibration.fit()

print(result.message)

print_model(calibration.model)

# Plot the calibrated smile for all maturities and save as PNG

fig = calibration.plot_maturities(max_moneyness=1.5, support=101)

fig.update_layout(title="BNS Calibrated Smiles")

fig.write_image(assets_path("bns_calibrated_smile.png"), width=1200)

Two-factor BNS¶

The original multi-factor BNS extends the single-factor model by replacing the variance with a convex combination of independent Gamma-OU processes. With weight \(w \in [0, 1]\) and a single Brownian motion driving the diffusion,

Pairing a fast-mean-reverting factor with a slow one decouples the short-maturity skew from the long-maturity level, in the same spirit as the DoubleHeston extension of Heston.

BNS2Calibration fits nine parameters:

[v01, v02, theta, beta, kappa2, kappa_delta, rho1, rho2, w]

with kappa1 = kappa2 + kappa_delta enforcing that the first factor

mean-reverts faster than the second.

Following the BNS superposition-of-OU construction, both factors share the same Gamma stationary marginal: the intensity and decay of the BDLP are tied across factors so that \(v^1\) and \(v^2\) have the same long-run distribution. Only the timescales and the leverages differ between the two factors.

Tying \((\theta, \beta)\) removes a well-known degeneracy between the marginal-distribution parameters and the timescales, and shrinks the search space without losing skew flexibility. The leverages \(\rho_1, \rho_2\) stay independent because the empirical equity skew flattens with maturity, which a single shared leverage cannot reproduce.

There is no warm start, so the optimiser begins from the user-supplied

initial parameters. Pick distinct timescales for bns1 and bns2 (and

consider opposite-sign leverages) to seed a meaningful two-factor fit.

Calibrated parameters¶

xtol termination condition is satisfied.

{

"bns1": {

"variance_process": {

"rate": 0.08122035325346619,

"kappa": 7.191909464718675,

"bdlp": {

"intensity": 1.6462966806854196,

"jumps": {

"decay": 7.633068371939248

}

}

},

"rho": -0.2590721628818859

},

"bns2": {

"variance_process": {

"rate": 0.4809913689821148,

"kappa": 0.1601559556419755,

"bdlp": {

"intensity": 1.6462966806854196,

"jumps": {

"decay": 7.633068371939248

}

}

},

"rho": 0.899999830215215

},

"weight": 0.9999566565848343

}

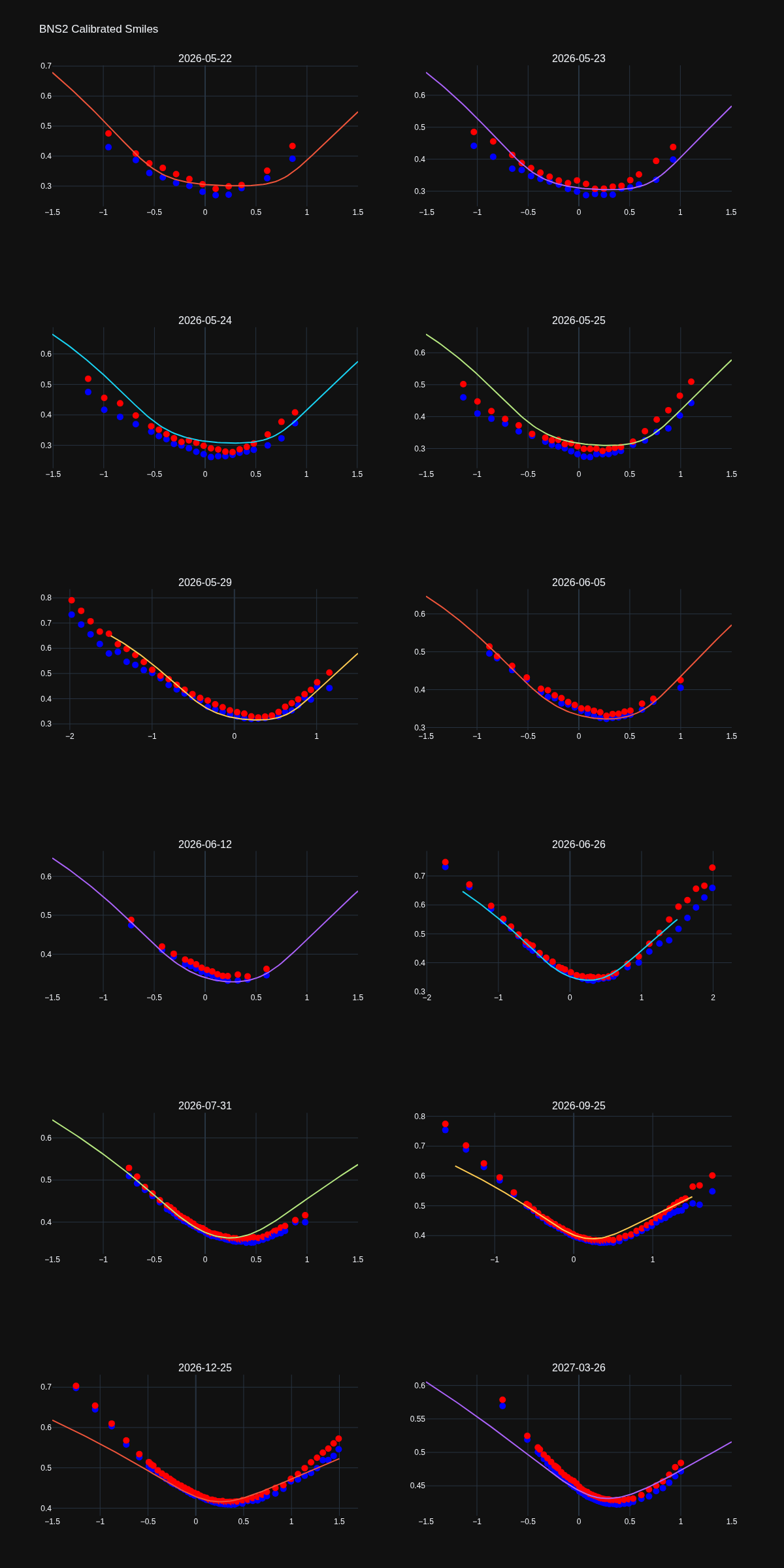

The two-factor variant adds flexibility on the term structure: the fast factor absorbs short-dated skew while the slow factor anchors the long end.

The remaining short-maturity gap is structural in the same way as the single-factor case. BNS2 still injects jumps only through the variance process, so the log-price wings are bounded by the jump sizes scaled by \(|\rho_i|\).

Code¶

import json

from docs.examples._utils import FIXTURES, assets_path, print_model

from quantflow.options.calibration import BNS2Calibration

from quantflow.options.calibration.base import ResidualKind

from quantflow.options.pricer import OptionPricer, OptionPricingMethod

from quantflow.options.surface import VolSurface, VolSurfaceInputs, surface_from_inputs

from quantflow.sp.bns import BNS, BNS2

# Load a saved volatility surface snapshot and build the surface

with open(FIXTURES / "volsurface_btc.json") as fp:

surface: VolSurface = surface_from_inputs(VolSurfaceInputs(**json.load(fp)))

surface.bs()

surface.disable_outliers()

# Two-factor BNS: a fast factor for short maturities and a slow one for long.

# Both factors share the same Gamma stationary marginal (vol, decay) following

# the BNS superposition-of-OU construction; only the timescale (kappa) and

# leverage (rho) differ. Opposite-sign leverages lets one factor lift the

# OTM-call wing (rho>0) while the other carries the equity-style downside

# skew (rho<0).

pricer = OptionPricer(

model=BNS2(

bns1=BNS.create(vol=0.45, kappa=20.0, decay=10.0, rho=-0.6),

bns2=BNS.create(vol=0.45, kappa=0.3, decay=10.0, rho=0.3),

weight=0.5,

),

method=OptionPricingMethod.COS,

)

calibration: BNS2Calibration[BNS2] = BNS2Calibration(

pricer=pricer,

vol_surface=surface,

moneyness_weight=0.3,

residual_kind=ResidualKind.IV,

)

result = calibration.fit()

print(result.message)

print_model(calibration.model)

fig = calibration.plot_maturities(max_moneyness=1.5, support=101)

fig.update_layout(title="BNS2 Calibrated Smiles")

fig.write_image(assets_path("bns2_calibrated_smile.png"), width=1200)